"In co-creation, strategy formulation involves imagining a new value chain that benefits all players in the ecosystem."

Venkat Ramaswamy and Francis Gouillart (2010)

Abstract

In this article, we apply the concept of value co-creation to the analysis of linkages between organizations and their human and financial resources to observe the emergence of cooperative activities in a specific innovation system. Through visual network analysis of a federated and socially constructed dataset of organizations and their related actors, we show how co-creation occurs through financial linkages.

We use the ecosystem concept as a metaphoric reference to value co-creation with a network-centric mindset. Business financing linkages reveal convergence and co-creation in the innovation ecosystem, and network analysis is used to visualize the relationships between firms. Through the lens of relationship-based synergy, we provide a snapshot of innovation funding, which highlights the collaboration of venture capital and government agencies in co-creating the emerging Finnish innovation ecosystem.

Introduction

The term co-creation was coined to explain emerging relationships between customers and the companies though which they were jointly creating value. Recently, the frame of reference has been extended to an emerging business and innovation paradigm that leads to the need of “changing the very nature of engagement and relationship between the institution of management and its employees, and between them and co-creators of value - customers, stakeholders, partners and other employees” (Ramaswamy, 2009).

Strategic value creation networks can be observed through network analysis of small, medium, and large enterprises, and they are important examples of co-creation. A leading idea in open innovation is that, because valuable knowledge exists outside of an individual organization, companies purposively co-create value networks through vendor-supplier relationships and collaborative service offerings that are specific to market segments. Inter-firm relationships created by the participation of executives and board members in two or more enterprises with related missions, markets, products, or social initiatives are additionally a potentially powerful force for value co-creation. In a similar way, enterprises receiving investment resources from the same financial source may share complementary visions of the future, complementary benefits from new technologies, and synergistic market development. Business ecosystems are comprised of the aggregate of these relationships among individuals and groups of individuals in clusters of companies. The competitive advantage of clusters accrues from the linkages and the synergy between activities (Porter, 2000).

Co-creation is an essential force in a dynamic innovation ecosystem because a continual realignment of synergistic relationships of people, knowledge, and resources is required for growth of the system and responsiveness to changing internal and external forces (Rubens, et al., 2011). On one hand, venture capital is the “independent, professionally managed, dedicated pools of capital that focus on equity or equity-linked investments in privately held, high growth companies” (Gompers and Lerner, 2001), has specific termination objectives that drive investments. On the other hand, government development agencies are often framed around capacity building missions – building markets, standards, supply chains, and technical and managerial talent. The investment strategies of development agencies vary in outcome objectives, as well as in time frame and financial objectives. For examples, differences in the “cultivation vs. harvesting” strategies evidenced by investments into and out of China have been described (Rubens et al., 2011).

Jungman and Seppä (2004) differentiate the role of angel investors, incubators, advisors, and corporate investments in bridging the gap between seed funding of prospective companies and capital infusion into investable companies. While all these types of financial resources may be available for business investment in a region, the role and proportion may vary. Investors’ ultimate objective is for a new company to undergo the major liquidity event that allows it to become listed on a stock exchange. An ecosystem including both experiential and financial resources is needed to co-create successful journeys across the gap from a prospective to a listable company.

In this article, we use data-driven social network visualization to present a network analysis of venture funding in the Finnish innovation ecosystem. A socially constructed dataset is used to study the nature of business co-creation through syndicated venture capital investments. We show that the dataset can be explored to provide value to researchers as well as ecosystem facilitators and other agents of change. The snapshot of innovation funding in Finland is examined by means of network analysis to visualize inter-firm relationships, following the ecosystem as metaphoric reference for value co-creation in a network-centric mindset. The analysis concentrates on investments of venture capital, which in Finland have been oriented to early equity-phase financing of high-tech startups. A total, all-inclusive analysis of the Finnish system is outside of the scope of this article, but the visualization snapshot of venture funding will serve as a starting point to stimulate the development of insights relevant to innovation experts, analysts, and decision makers within the context of the Finnish innovation ecosystem.

Venture Funding for the Finnish Innovation Ecosystem

The Finnish national innovation system has been described as a network of various actors, with education, research, product development, and knowledge-intensive business and industry at its core. Regarding the flows of investments into this system, it has been noted that “because of the importance of the public venture capital/private equity organizations, the Finnish venture capital system can be described as dual one in which some private venture capital funds have been initiated by public intervention” (Luukkonen, 2006). Furthermore, special characteristics have been noted: i) due to the small markets in Finland, the growth expectations oftentimes have been limited, which has impacted non-Finnish investors’ perceptions of the attractiveness of investment in Finnish companies; ii) these existing public investors many times have been passive; and iii) that there are very few corporate venture capitalists in Finland (Luukkonen, 2006).

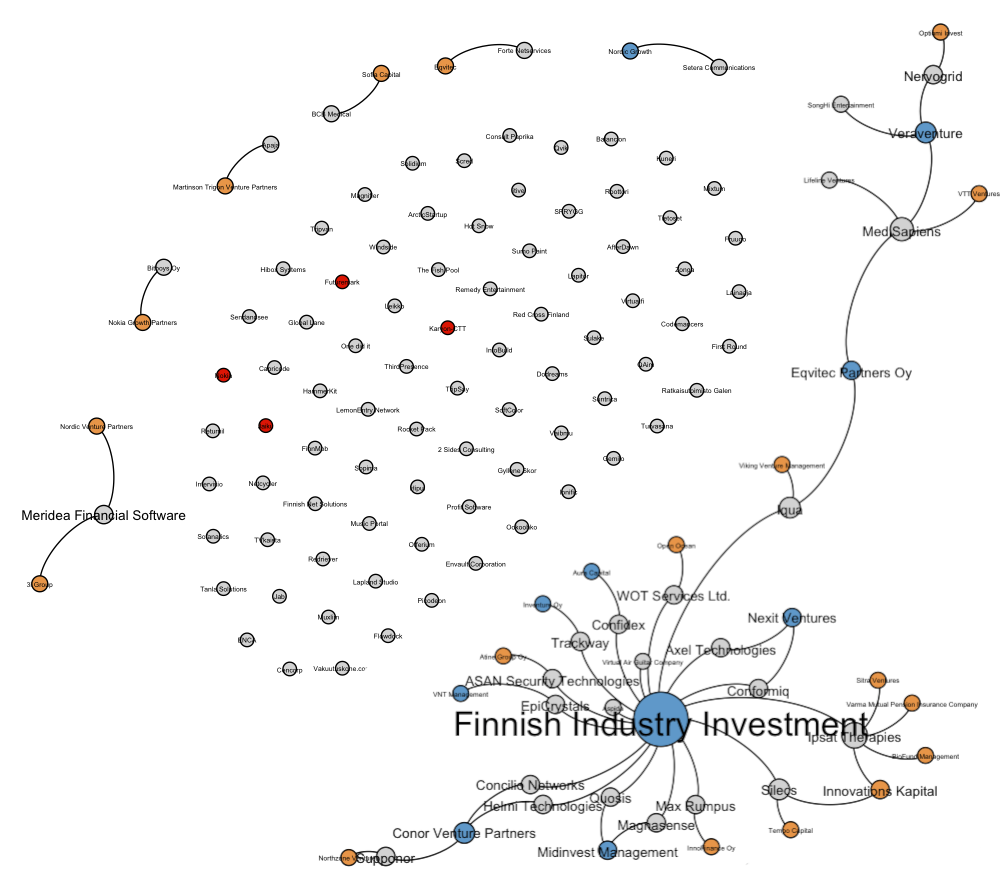

In this sample of 108 high-tech companies, 53 investments were announced from 28 institutional investors, made in 29 rounds between 2005 and 2010. An examination of the social networks and other structures produced from this data is much like a walkabout in the Finnish innovation funding ecosystem. Visual analysis shows the patterning of connections between company actors as well as those of financial resources flowing to Finnish technology-based companies, implying co-creation from innovation funding. For example, the walkabout reveals a landscape of four companies that have come of age – sold or issued an initial public offering (IPO), amidst many independent firms – and a few with international connections. One actor dominates the investment landscape.

Figure 1. Network of Finnish Technology Companies and their Investment Organizations

Figure 1 shows all 136 actors in our sample, which consisted of 108 technology-based companies with a home office in Finland and 28 investment organizations. Companies and their funding organizations are interconnected with edges. The actors are colour-coded: companies are gray, unless they were sold or have issued IPO, in which case they are red. Investors with their home office in Finland are blue; investors whose whereabouts are international or unknown in the dataset are orange. The nodes are inflated according to their degree (i.e., the number of connections that they have to other nodes): the bigger the node, the more connections it has.

Among the notable relationships in the sample, Figure 1 shows:

-

Ipsat Therapies, Medisapiens, Iqua, and Silecs have the largest number of connections to investors.

-

Finnish investment organizations represent roughly half of the investors for these Finnish companies.

-

Conor Venture Partners, Veraventure, Eqvitec Partners, Innovations Kapital, Midinvest Management, and Nexit Ventures are linked to more than one company by their investments.

-

Biofund Management, Sitra Ventures, Varma Mutual Pension Insurance Company (Varma), and Finnish Industry Investment invested in Ipsat Therapies. This was the first investment in the sample and occurred in April 2005.

-

Medisapiens received investment from VTT Ventures, Eqvitec Partners, Veraventure, and Lifeline Ventures. This was the most recent investment and occurred in June 2010.

-

Most of the companies (75%) in this sample are not receiving funding from an investment organization. Although some companies have investments from individuals, angel investors are not included in this analysis.

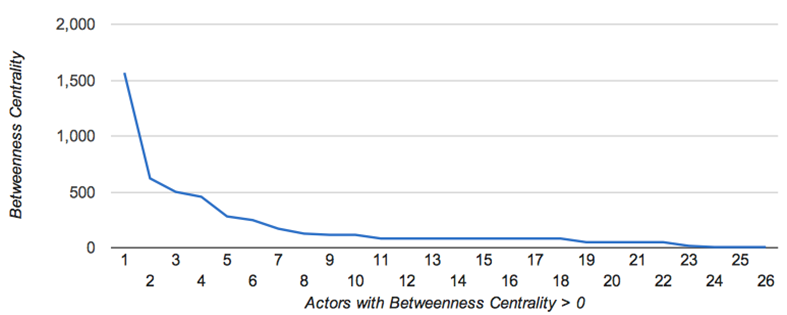

In our sample, 56 of the companies and investment organizations (41%) are connected to one or more actors. Figure 2 shows the betweenness centrality values for the 26 actors that have a value larger than zero. Betweenness centrality is one of the key metrics in social network analysis. It is based on counting the number of times that a given node is included in the shortest path between two nodes. Of the companies, Iqua has the largest betweenness centrality value: 610. Of the investment organizations, government-owned Finnish Industry Investment is connected to the largest number of companies, with a betweenness centrality value of 1557. For the whole sample, including the actors with no connections, betweenness centrality values of the lowest, low-medium, and upper medium quartiles are zero, making the average value 36.

Figure 2. Distribution of Betweenness Centrality

The value distribution of betweenness centrality roughly follows a power law. Node degree value, the number of connections per actor, has a similar kind of distribution. This suggests that the network is scale free – characterized by a very small number of nodes that are highly connected and many nodes with little connection (Barabási and Bonabeau, 2003). In scale-free networks, growth patterns that show preferences for attaching to highly connected nodes are typical and generally lead to the development of hubs (i.e., nodes with an enormous number of links) in a rich-get-richer manner. Scale-free networks tend to be “robust against accidental failures but vulnerable to coordinated attacks” (Barabási and Bonabeau, 2003).

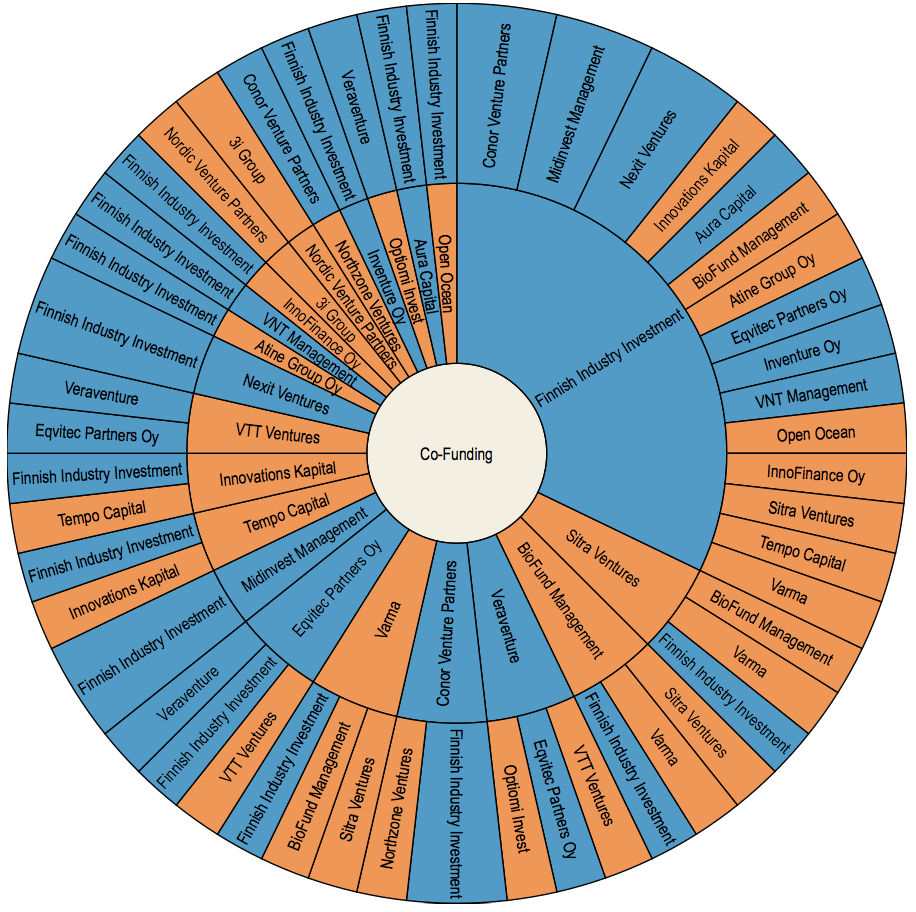

Through the companies they co-fund, relationships between investment organizations are of strategic interest for co-creation. Sunburst diagrams were applied to visualize patterns in the Finnish innovation ecosystem. Figure 3 shows the co-investments of 22 investment organizations into 19 Finnish companies. Each investor that co-invested with another investor in this sample is shown in the inner circle. Their co-investors are placed in the outer circle adjacent to each investor, without specification of the time of investment. In this design, each investor appears as co-investor at least two times in the diagram. Investment organizations identified as Finnish are shown in blue. The Finnish Industry Investment co-invested with 15 other funding organizations; some co-investors were Finnish, while the location of others was not available in the data. (It should be noted that some of the investors are known by the authors to be Finnish, but their Finnish locations were not identifiable programmatically. The locations of these investors were therefore classified as unknown and are shown in orange in Figure 3. These organizations include, among others, Varma, Sitra Ventures, and VTT Ventures.)

Figure 3. Patterns of Co-Investing in Finnish Technology Companies

Figure 4 reveals funding paths or bursts for companies that have received two rounds of funding; no companies in this dataset were reported to have received a third-round investment. Second-round investors are shown on the outer circle adjacent to the investors of the first round for the same company. Finnish Industry Investment, for example, has been both a first-round investor and a second-round investor. When Sitra Ventures and Varma are regarded as being Finnish, we can see that a small majority (57%) of funding organizations participating in multiple funding rounds are Finnish organizations.

Figure 4. First and Second-Round Investment Paths in Finnish Technology Companies

Discussion

The approach for visual co-creation analysis presented here is a synthesis of visual social network analysis and data-driven information visualization. Visualization and measurement are claimed to be the two main factors enabling the explosive development of modern science. Visualization has been a key element of social network analysis - and its precursor, sociometry - in supporting the exploration, presentation, and analysis of the structure of communities. The general objective of information visualization is to amplify the cognition of a user through an expressive, often interactive view that gives insight on a given phenomena represented by the data.

Data-driven visual storytelling allows insights on the structure and dynamics of a network to be shared with the help of visualizations. “[S]torytelling allows visualization to reveal information as effectively and intuitively as if the viewer were watching a movie” (Gershon & Page, 2001). Hans Rosling gives particularly inspiring examples of such storytelling; his presentations are sometimes referred as “the best stats you've ever seen” (TED Talks, 2006)

This study’s visual social network analysis revealed structural connections between Finnish technology-based companies and their investment organizations. A significant proportion of Finnish companies in the high-tech sector have not received funding from investment organizations since 2005. For those Finnish companies that have received funding, 63% of have received either first or second-round funding from Finnish Industry Investment. A handful of investment organizations (some Finnish and some not) provide modest diversification to the Finnish funding landscape, which shows a scale-free pattern.

Further, this analysis has generated preliminary insights about the general patterns of co-creator networks supporting the Finnish innovation ecosystem in the high-tech sector. The sunburst visualizations display funding pathways and highlight the flexibility of Finnish government investment organizations to co-create in both first-round and second-round funding. The co-creation role of these organizations is visualized through both concurrent and sequential cooperative investments. At the same time, the visualizations also reveal a dependency on Finnish Industry Investment and an opportunity to further diversify institutional investments in Finnish companies.

These initial patterns suggest avenues for future study. Investment relationships reflect an intentional alignment of business resources and goals that may be based on technologies, markets, or globalization strategies. A resource-based relationship implies that the partners share objectives, share risks, and share rewards as they co-create value through investments. In co-creation, both the risks and rewards are shared; however they may not be equal. The roles of first and second-round investors may be specialized with respect to the amount of risk, the financial and temporal objectives for exit, and the value of the network itself. Across public and private Finnish organizations making investments in technology-based companies with headquarters in Finland, this study showed that Finnish Industry Investment is unique in both leading and following the investments made by other entities.

This study lacks two very important investment players for a full view of the Finnish innovation ecosystem. Since firms were used as the unit of analysis, individuals serving as angel investors were not included. In a subsequent study, we seek to gain further insight on the business angels’ vital role in seed financing for new technology-based companies – an act of co-creation in this sense. An interesting, though difficult, task for future work is visualizing the role of incubators and business angels in closing the gap between venture and capital.

Further studies could include the utilization of temporal data, which often yields insights about the evolution of a network. Network visualization tool-development initiatives such as Gource and Gephi are clear indicators of the interest that the open source community has in temporal network visualization. These tools are of high value when the dynamics of innovation ecosystems are studied for insights on trends, the roles of different actors, diffusion of information and innovations et cetera, but they insist on the availability of rich data sources.

Conclusion

Applying information visualization and visual social network analysis has huge potential for revealing the social structures and network dynamics within innovation ecosystems, from individual organizations to the whole world. Despite recent rapid development of visual tools for social network analysis, one major issue that hinders data-driven visual analysis of co-creator networks in innovation ecosystems is the lack of accessible, timely data about the global ecosystem of high-tech companies. We anticipate development in this area in the near future with the advent of (open) linked data (see http://linkeddata.org), which is currently endorsed with respect to opening up public administration. The authors are contributing to this opportunity by creating a dataset representing high-tech companies and building up research methods for this dataset.

The scale-free patterning of the Finnish venture capital network is similar to the findings of Barabási (2010) who claims that such patterning can be found in nearly all kinds of human activities. Adding the temporal dimension to data enables the analysis of the evolution of the network. This opens up a new level of insights into changes in the network that, at best, supports the formulation of future scenarios for agents of change in different innovation ecosystems. Two important opportunities for innovation policy analysts concern identifying incentives to effectively encourage the reinvestment of exit resources and orchestrating mechanisms to strategically encourage global participation in a manner that provides a return on investment back to its origin.

This article is based on a paper presented in EBRF 2010: Co-Creation as a Way Forward. The authors express their gratitude to the Venture Capital Industry, Business Angels, and Knowledge Investors session chairs Prof. Markku Maula, Prof. Marko Seppä, and Dr. Jennifer Walske, as well as the other participants of EBRF 2010 for their co-creation efforts contributing to the article. Camilla Yu provided valuable feedback for revising the article. For additional versions of these visualizations, please refer to http://bit.ly/fininnofin.